Familiarizing yourself with invoice factoring requirements before applying can improve your approval odds and ensure you aren’t surprised by anything during the process. Below, we’ll cover how factoring works and what to expect when you apply, so you’re better prepared for the journey.

Invoice Factoring Background and Benefits

Before we dig into invoice factoring requirements, let’s quickly review how factoring works.

Invoice Factoring Definition

Invoice factoring is a business funding method where a company sells its unpaid invoices to a factoring company at a discount. The factoring company advances up to 95% of the invoice’s value and collects payment directly from the company’s client. The remaining sum is then sent to the business minus a small factoring fee. If you’re considering this funding option, understanding the cost of factoring is crucial to evaluating how fees and rates might impact your cash flow strategy, especially for those exploring factoring for service providers. It’s also important to understand whether your factoring agreement will use notification or non-notification factoring, as this determines if your clients are informed that a third party is managing invoice collection.

For businesses struggling to meet payroll obligations, payroll factoring can provide fast access to working capital, ensuring employees are paid on time without cash flow disruptions.

Benefits of Invoice Factoring

There are many benefits to invoice factoring. A few of them include:

- Easy Approval: Most businesses qualify for invoice factoring. Applications are typically processed within a day or two.

- Fast Payouts: Factoring companies usually pay via ACH, so money reaches the business’s bank account within two business days. Faster methods are sometimes available, too.

- Debt-Free Funding: There’s no debt to pay back with factoring because your client clears the balance when they pay their invoice.

- Flexibility: You’re in control of which invoices you factor, so you also have more control over costs and can keep more money in your pocket.

- Collections: Factoring companies collect the balance for you, so you’re freed from chasing invoices.

- Value-Added Services: Additional services vary depending on your factoring partner. However, some will generate invoices for you, provide other forms of funding, or provide extra services to help strengthen your business.

Businesses in the construction industry often face cash flow challenges due to delayed payments and upfront project costs, making construction factoring an ideal solution to keep projects moving smoothly.

Given that the typical Canadian business waits an average of 53 days for B2B payments, per Atradius research, factoring is an excellent way to accelerate payment while maintaining strong customer relationships. Factoring is also often viewed as an alternative to business loans since it provides a cash injection and can fill cash flow gaps.

Invoice Factoring Approval

It’s important to note that “approval” is best viewed as a three-stage process, even though it’s rarely described as such.

- Business Approval: The first stage is getting your business approved for factoring. Again, most businesses are approved. This is more of a verification process to ensure your business operates legally and is stable. This can be completed within one or two business days.

- Client Approval: The second stage involves confirming your individual accounts or clients are approved and to what degree. Only accounts with invoices you intend to submit for factoring must undergo this process. This is often performed as part of the initial business approval, though you can submit accounts later as needed, too.

- Invoice Approval: The final stage involves approving individual invoices. This is more of a quick verification to ensure the invoice you’re submitting is authentic. Some factoring companies leverage special technology that automatically approves invoices, while others perform the task manually. In these cases, it usually takes less than a day.

These concepts are broken down further as the overall invoice factoring requirements are explored below.

6 Common Invoice Factoring Requirements

Now that you’re familiar with the basics, let’s look at invoice factoring requirements you’ll need to meet to get approved.

1. Documentation

One of the first things factoring companies will ask for are standard legal and financial documents related to your business. These confirm that your company is established, operates legally, and has adequate cash flow.

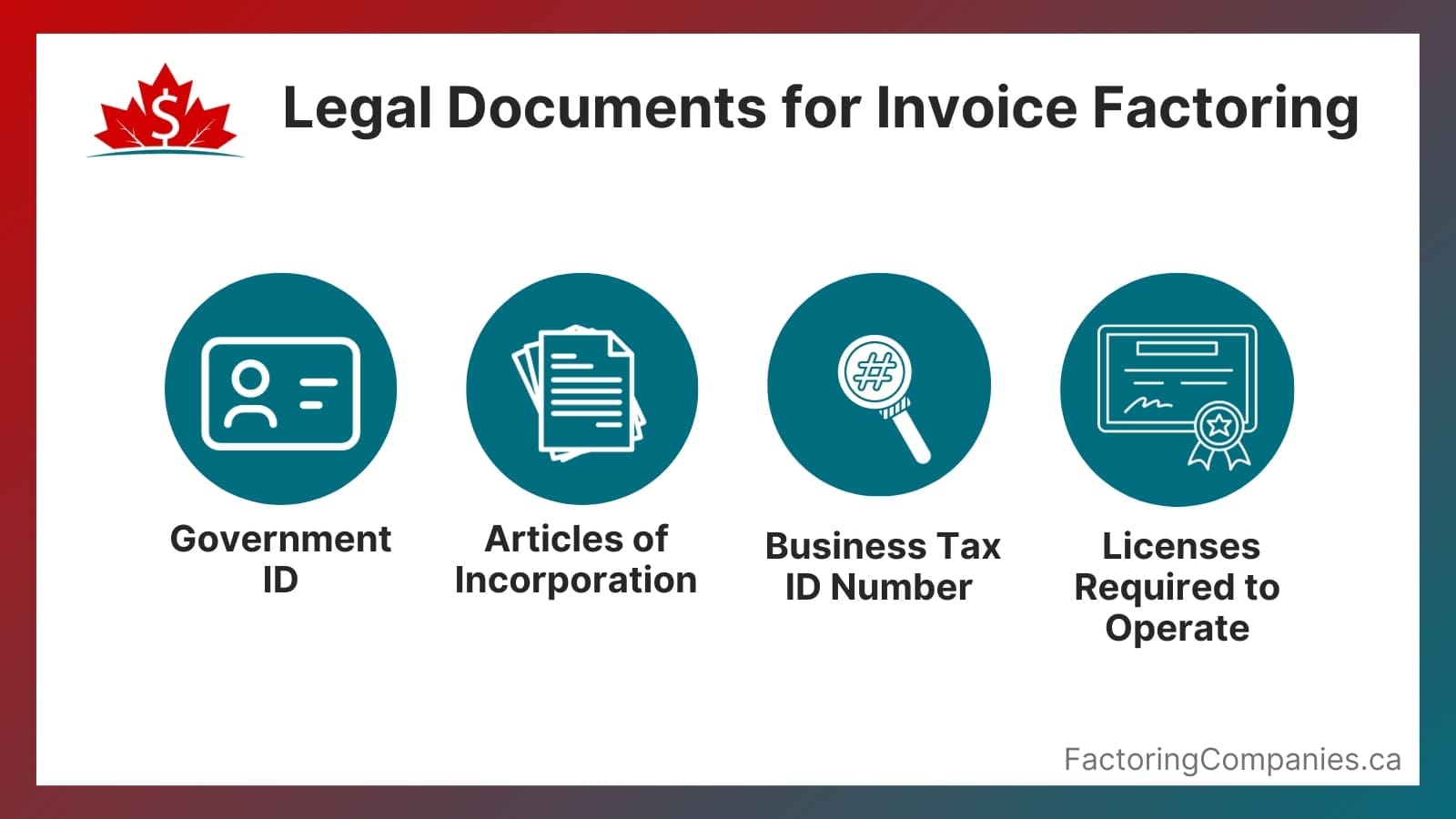

Legal Documents for Invoice Factoring

- Your Government-Issued ID

- Articles of Incorporation

- Business Tax ID Number

- Licenses Required to Operate

Financial Statements for Invoice Factoring

- Accounts Receivable Aging Report

- Bank Statements

- Tax Statements

2. Clear and Unpaid B2B or B2G Invoices

Although some factoring companies work with B2C invoices, most only work with businesses that serve other businesses and government contractors. You’ll need invoices that clearly show essential info, such as client details, the reason for the balance, the total balance, and the due date.

Invoice Verification for Factoring

Once your business is approved for factoring, each invoice you factor will be reviewed to ensure it’s valid. Factoring companies can often verify invoices with the information they have and a copy of the invoice, though sometimes they need to speak with the company or government agency responsible for paying the invoice to ensure that it’s valid.

3. Creditworthy Clients

Even businesses that haven’t established credit or don’t have good credit can qualify for invoice factoring. This is because your clients are the ones paying the invoices, so their credit matters more than yours. If you’re asking, do factoring companies do credit checks? The answer is yes, but they typically evaluate your clients’ creditworthiness, not your business’s.

Client Creditworthiness in Invoice Factoring

Invoice factoring companies run credit checks on your clients to ensure they’re likely to pay their invoices in a timely manner. Your factoring company will also provide you with a maximum factoring amount for each client to help minimize the risk of non-payment. For instance, you may be told that you can safely extend $50,000 in trade credit to one client and $100,000 to another.

You remain in control of which clients you work for and how much credit you extend. However, any invoices that exceed these levels established for risk mitigation won’t be eligible for factoring.

4. Absence of Legal Encumbrances or Liens

An entity that has a claim to your assets can place a lien on them. For instance, a lien is generally placed on the property if you take out a mortgage. It means the lender can pursue liquidating the property if you don’t pay your loan. These types of liens are generally not an issue for factoring.

However, sometimes liens can be placed on your receivables. This might happen if:

- You didn’t pay the bills, and a court allowed the lien to be placed

- You’ve already used your receivables as collateral

- You’re behind on tax payments

Sometimes, you can ask the lien holder to release the lien, and they’ll do it because it makes it easier for you to pay them back. This is somewhat common with tax-related liens. Other times, you’ll need to pay off your balance in full or pursue other legal means to remove a lien before you can factor your invoices.

5. Positive Business Operations and Reputation

Factoring companies will also look into your reputation before agreeing to factor invoices. For the most part, they’ll confirm no illegal behaviour is occurring that might put your business at risk.

6. Appropriate Invoice Terms and Amounts

A final concern is whether your invoices are appropriate for factoring. Each company will have different guidelines in this respect, and some will have different rules for each industry. For instance, some will factor invoices that are as little as $5,000 or $10,000, while others have higher minimums. Some will factor invoices valued as high as $500,000, while others set a lower ceiling.

Factoring companies also prefer to work with newer invoices. For instance, some will only accept invoices that are less than 30 days old, while others have a 90-day age limit. Additionally, businesses operating in Canada must adhere to specific Canadian invoice factoring regulations when engaging in invoice factoring to ensure compliance and avoid legal complications.

You’ll want to confirm these details with any factoring company you’re considering partnering with.

Begin the Approval Process and Get a Free Rate Quote

Your invoice factoring company will walk you through their process, but it’s helpful to have your documents ready in advance to speed things up. Request a complimentary factoring quote to get started.

About Factoring Companies Canada

Accounting Software for Small Business: 5 Things to Look For

Accounting Software for Small Business: 5 Things to Look For 6 Options for Financing Your Startup Staffing Agency

6 Options for Financing Your Startup Staffing AgencyRelated Insights

Get an instant factoring estimate

Factoring results estimation is based on the total dollar value of your invoices.

The actual rates may differ.

CLAIM YOUR FREE FACTORING QUOTE TODAY!

PREFER TO TALK?

You can reach us at

1-866-477-1778

Get an instant factoring estimate

Factoring results estimation is based on the total dollar value of your invoices.

The actual rates may differ.

CLAIM YOUR FREE FACTORING QUOTE TODAY!

PREFER TO TALK? You can reach us at 1-866-477-1778